[GUEST ACCESS MODE: Data is scrambled or limited to provide examples. Make requests using your API key to unlock full data. Check https://lunarcrush.ai/auth for authentication information.]  LTValue [@qualitybargain](/creator/twitter/qualitybargain) on x 2238 followers Created: 2025-07-16 12:01:09 UTC Kortek Corp $052330.KS - showed up on a NCAV screen, looked interesting after reading for 30mins so sharing here. Microcap Korean net-net. Market cap US$123m, float XX% of sh/out. Market cap today is XX% of NCAV with cash being XX% of NCAV. Current debt KRW 33.3bn, non-current KRW 5.6bn against cash of KRW 99.5bn. Also has KRW 35.6bn of short-term deposits not incl. in cash equivalents. Manufactures industrial monitors for casino slot machines (has had global #1 market share for XX consecutive years), as well as medical, retail/advertising, and aviation control centres. Unsure of the mix. Most products are made to order with production facilities in Songdo, Korea and Hanam, Vietnam. Monitors are XX% of sales mix, rest is aftermarket services. That's all it does. Pretty simple business. Website has some good info on what the business does and corporate history. Financials are all in Korean so have to do some translating to make them legible. Don't have much experience looking at Korean stocks so this was challenging but made it work. FY24 gross margin was 24%, has hovered ~16-25% last several years. EBITDA also fluctuates but business seems to have stabilised at ~HSD margin. LTM PE is 4.4x. Profitability was impacted in FY20-21 due to COVID but otherwise has been consistently profitable since 2014. Fundamentals are improving. In 3m to March 2025, revenue +17.3% y/y with significant leverage on operating income +209% y/y. Below line items like finance income and associate income moved around but profit still +42%. Has also been buying back shares, did KRW 5.6bn from 17th March 2025 to XX May 2025 (~3% of market cap). Stock up ~30% YTD. Can't buy it through IBKR so have no position. Haven't done further work but on surface level, looks like an ok business, cheap valuation on both earnings and balance sheet, and returning capital to shareholders.  XXX engagements  **Related Topics** [market cap](/topic/market-cap) [south korean won](/topic/south-korean-won) [debt](/topic/debt) [$123m](/topic/$123m) [microcap](/topic/microcap) [$052330ks](/topic/$052330ks) [Post Link](https://x.com/qualitybargain/status/1945453648290746532)

[GUEST ACCESS MODE: Data is scrambled or limited to provide examples. Make requests using your API key to unlock full data. Check https://lunarcrush.ai/auth for authentication information.]

LTValue @qualitybargain on x 2238 followers

Created: 2025-07-16 12:01:09 UTC

LTValue @qualitybargain on x 2238 followers

Created: 2025-07-16 12:01:09 UTC

Kortek Corp $052330.KS - showed up on a NCAV screen, looked interesting after reading for 30mins so sharing here.

Microcap Korean net-net. Market cap US$123m, float XX% of sh/out. Market cap today is XX% of NCAV with cash being XX% of NCAV. Current debt KRW 33.3bn, non-current KRW 5.6bn against cash of KRW 99.5bn. Also has KRW 35.6bn of short-term deposits not incl. in cash equivalents.

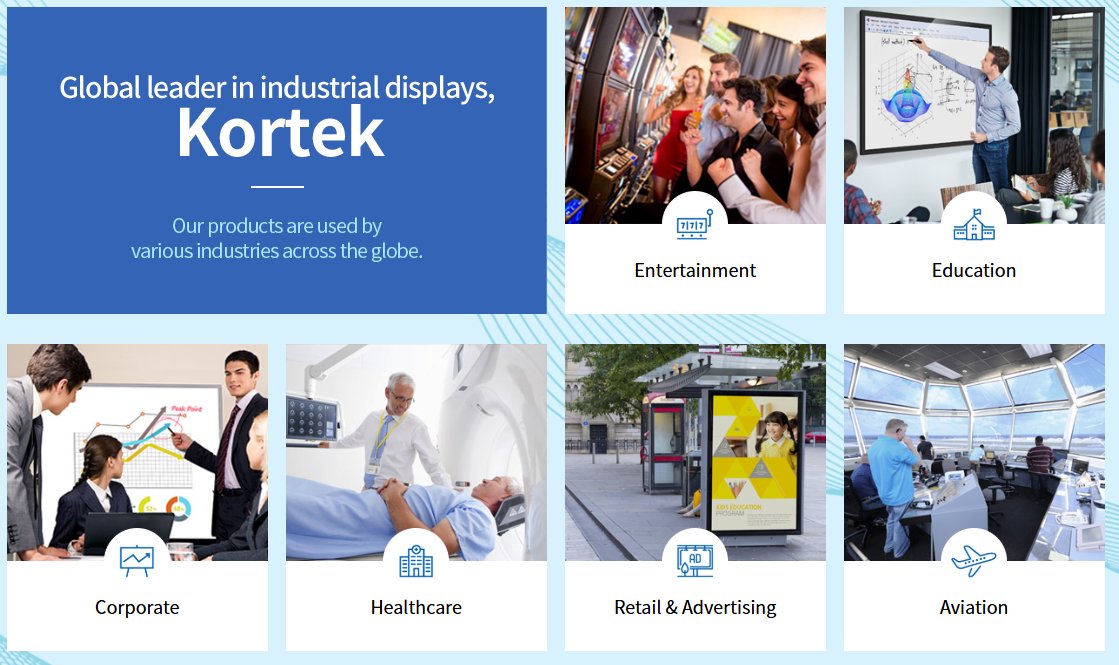

Manufactures industrial monitors for casino slot machines (has had global #1 market share for XX consecutive years), as well as medical, retail/advertising, and aviation control centres. Unsure of the mix. Most products are made to order with production facilities in Songdo, Korea and Hanam, Vietnam. Monitors are XX% of sales mix, rest is aftermarket services. That's all it does. Pretty simple business.

Website has some good info on what the business does and corporate history. Financials are all in Korean so have to do some translating to make them legible. Don't have much experience looking at Korean stocks so this was challenging but made it work.

FY24 gross margin was 24%, has hovered ~16-25% last several years. EBITDA also fluctuates but business seems to have stabilised at ~HSD margin. LTM PE is 4.4x. Profitability was impacted in FY20-21 due to COVID but otherwise has been consistently profitable since 2014.

Fundamentals are improving. In 3m to March 2025, revenue +17.3% y/y with significant leverage on operating income +209% y/y. Below line items like finance income and associate income moved around but profit still +42%.

Has also been buying back shares, did KRW 5.6bn from 17th March 2025 to XX May 2025 (~3% of market cap). Stock up ~30% YTD.

Can't buy it through IBKR so have no position. Haven't done further work but on surface level, looks like an ok business, cheap valuation on both earnings and balance sheet, and returning capital to shareholders.

XXX engagements

Related Topics market cap south korean won debt $123m microcap $052330ks