[GUEST ACCESS MODE: Data is scrambled or limited to provide examples. Make requests using your API key to unlock full data. Check https://lunarcrush.ai/auth for authentication information.]  LTValue [@qualitybargain](/creator/twitter/qualitybargain) on x 2231 followers Created: 2025-07-10 07:37:41 UTC Been doing some work on $UBER recently. Interesting to see how some of the Street doesn’t model cash tax properly or account for it in valuation. Uber, after years of losses, turned GAAP profitable for the first time in 2023, and more meaningfully so in 2024. In the 10k, they disclose ~$10.6bn of US federal/state NOLs and R&D credits. The majority are now considered 'more likely than not' to be realisable, and most have unlimited carryforward (i.e. no expiry date). There are also sizable Dutch NOLs but I'm ignoring those as they aren't confident in being able to use the majority of these. This means Uber’s cash tax rate will likely remain well below the statutory rate for years. Visible Alpha doesn’t show cash tax consensus, and BBG doesn’t either, so I had a look at a GSR model. There is a $412m drag on operating cash flow in FY25 due to valuation allowance reversal (a non-cash P&L tax benefit that gets subtracted in CFO under the indirect method, since it's a deferred tax adjustment), and no cash benefit at all from FY25-30 from using up the existing DTA balance. And no adjustment to EV for DTAs. All valuation is done off Adj. EBITDA and FCF multiples so the value of the cash tax shield is completely ignored. In my mini-DCF I assume a XX% cash tax rate. This results in $5.572bn of cash tax savings in FY25-29, based on my numbers. That aligns well with the $6.2bn DTA balance recognized in 2024 and so feels grounded in what’s already been booked. The present value of that discounted at X% is about 0.5x FY25 EBITDA, which is meaningful. It’s also ~HSD-LDD% of consensus FCF from FY26–29, just from tax. That's a meaningful source of variant perception vs. market numbers. Just from tax! And that's just on what's already recognised and not including future NOLs. Good lesson here in the value of reading financial footnotes properly!  XXXXX engagements  **Related Topics** [$106bn](/topic/$106bn) [10k](/topic/10k) [tax bracket](/topic/tax-bracket) [$uber](/topic/$uber) [stocks technology](/topic/stocks-technology) [Post Link](https://x.com/qualitybargain/status/1943213017283596504)

[GUEST ACCESS MODE: Data is scrambled or limited to provide examples. Make requests using your API key to unlock full data. Check https://lunarcrush.ai/auth for authentication information.]

LTValue @qualitybargain on x 2231 followers

Created: 2025-07-10 07:37:41 UTC

LTValue @qualitybargain on x 2231 followers

Created: 2025-07-10 07:37:41 UTC

Been doing some work on $UBER recently.

Interesting to see how some of the Street doesn’t model cash tax properly or account for it in valuation.

Uber, after years of losses, turned GAAP profitable for the first time in 2023, and more meaningfully so in 2024.

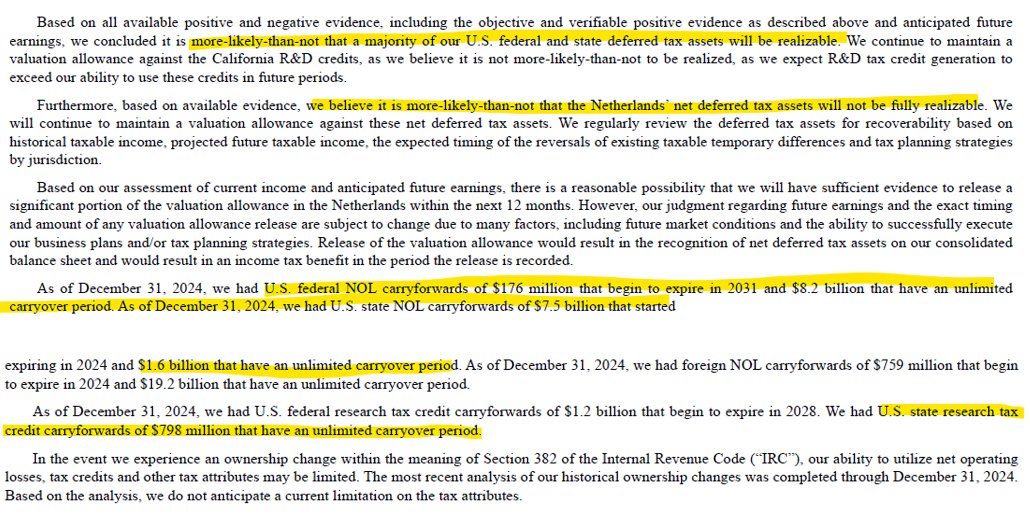

In the 10k, they disclose ~$10.6bn of US federal/state NOLs and R&D credits. The majority are now considered 'more likely than not' to be realisable, and most have unlimited carryforward (i.e. no expiry date). There are also sizable Dutch NOLs but I'm ignoring those as they aren't confident in being able to use the majority of these.

This means Uber’s cash tax rate will likely remain well below the statutory rate for years.

Visible Alpha doesn’t show cash tax consensus, and BBG doesn’t either, so I had a look at a GSR model.

There is a $412m drag on operating cash flow in FY25 due to valuation allowance reversal (a non-cash P&L tax benefit that gets subtracted in CFO under the indirect method, since it's a deferred tax adjustment), and no cash benefit at all from FY25-30 from using up the existing DTA balance. And no adjustment to EV for DTAs. All valuation is done off Adj. EBITDA and FCF multiples so the value of the cash tax shield is completely ignored.

In my mini-DCF I assume a XX% cash tax rate. This results in $5.572bn of cash tax savings in FY25-29, based on my numbers. That aligns well with the $6.2bn DTA balance recognized in 2024 and so feels grounded in what’s already been booked.

The present value of that discounted at X% is about 0.5x FY25 EBITDA, which is meaningful. It’s also ~HSD-LDD% of consensus FCF from FY26–29, just from tax. That's a meaningful source of variant perception vs. market numbers. Just from tax! And that's just on what's already recognised and not including future NOLs.

Good lesson here in the value of reading financial footnotes properly!

XXXXX engagements

Related Topics $106bn 10k tax bracket $uber stocks technology