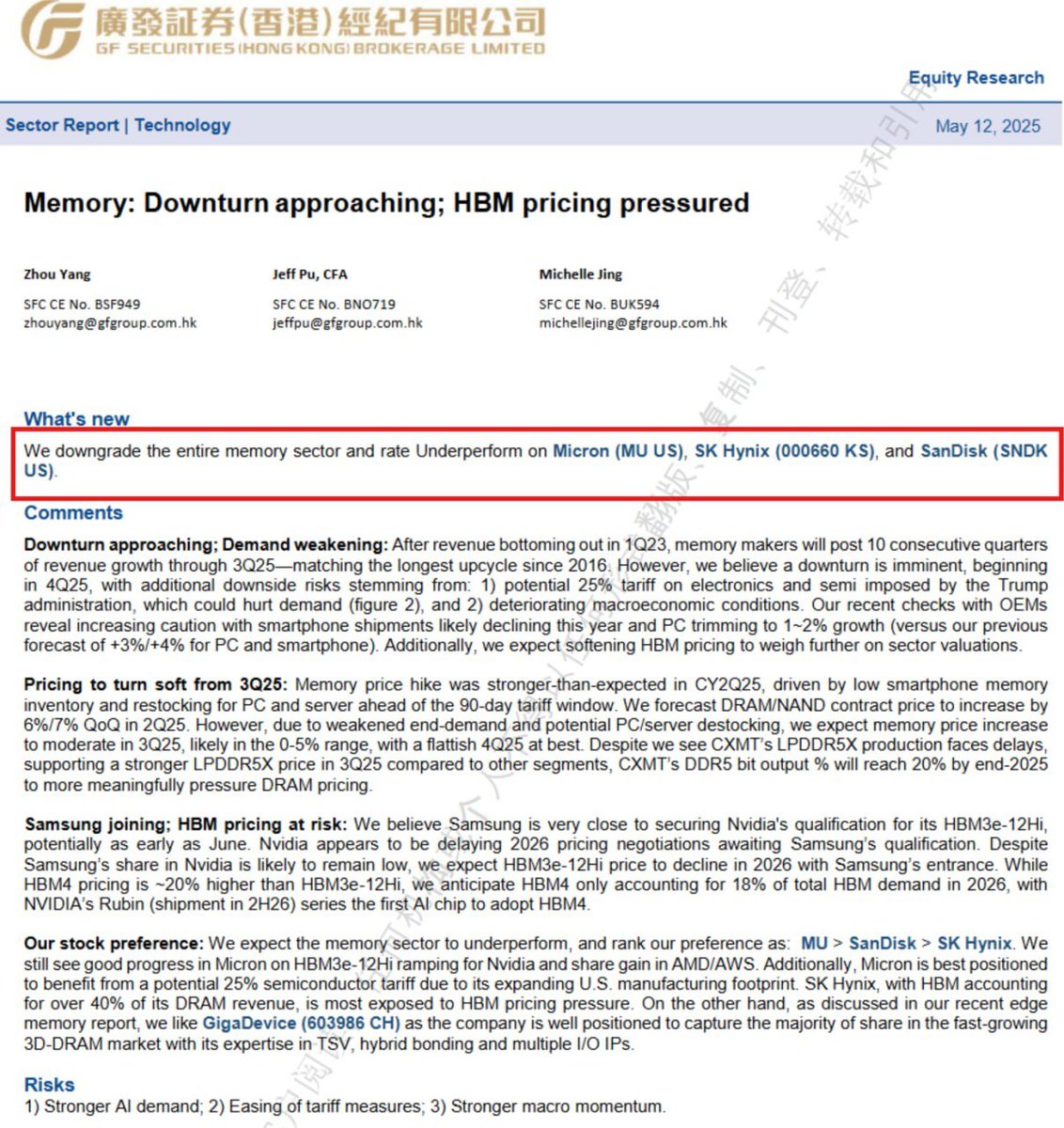

[GUEST ACCESS MODE: Data is scrambled or limited to provide examples. Make requests using your API key to unlock full data. Check https://lunarcrush.ai/auth for authentication information.]  Jukan [@Jukanlosreve](/creator/twitter/Jukanlosreve) on x 22.9K followers Created: 2025-05-12 03:32:25 UTC GF Securities – Memory Sector: Downturn Approaching, HBM Pricing Pressured – We downgrade the entire memory sector and assign an Underperform rating on Micron (MU US), SK Hynix (000660 KS), and SanDisk (SNDK US). ◾+ Sector slowdown and demand weakening intensifying – Following a bottom in 1Q23, the memory sector is projected to post XX consecutive quarters of improvement through 3Q25 — marking the longest upcycle since 2016. – However, a downturn is increasingly likely starting from 4Q25. Key reasons include: 1) Risk of a XX% tariff on electronics/semiconductors by the Trump administration 2) Deteriorating global macro conditions → smartphone shipment growth to turn negative, PC shipments limited to +1~2% 3) HBM pricing could also become a headwind ◾+ HBM and DRAM prices: Potential weakening from 3Q25 – As of CYQ2, memory pricing was stronger than expected (thanks to low smartphone inventories and preemptive restocking during the 90-day tariff waiver) – 2Q25 DRAM/NAND contract pricing: QoQ +67% expected – However, from 3Q25, price momentum is likely to slow due to weak demand and inventory pressure from servers and PCs: - Pricing increase of only around 0~5% or potentially flat - This flat trend may persist through 4Q25 ◾+ Samsung’s entry to intensify HBM market competition – Samsung is preparing to qualify HBM3e-12Hi with NVIDIA (possibly by June) – NVIDIA is delaying 2026 HBM3e pricing negotiations pending Samsung’s qualification – Samsung’s market entry in 2026 may trigger HBM4 price declines - Currently, HBM4 is priced at a XX% premium to HBM3e-12Hi - CXMT’s DDR5 production ratio also expected to reach XX% by end-2025 ◾+ Stock preference – 1st: Micron > 2nd: SanDisk > 3rd: SK Hynix - Micron: U.S.-based production → potential beneficiary of tariffs; gaining share in AMD/AWS - SanDisk: Focused on NAND → less exposed to HBM, relatively defensive - SK Hynix: Over XX% of DRAM revenue from HBM, but high exposure to HBM pricing pressure creates downside risk ✅ Conclusion: The memory sector is likely to peak in 3Q25, with a potential slowdown thereafter. HBM pricing headwinds and renewed U.S. tariff risk are expected to weigh on medium- to long-term valuations. Among covered names, Micron is viewed most favorably, while SK Hynix remains relatively conservative due to its large HBM exposure.  XXXXXX engagements  **Related Topics** [$000660ks](/topic/$000660ks) [rating agency](/topic/rating-agency) [$1776hk](/topic/$1776hk) [Post Link](https://x.com/Jukanlosreve/status/1921770409927549247)

[GUEST ACCESS MODE: Data is scrambled or limited to provide examples. Make requests using your API key to unlock full data. Check https://lunarcrush.ai/auth for authentication information.]

Jukan @Jukanlosreve on x 22.9K followers

Created: 2025-05-12 03:32:25 UTC

Jukan @Jukanlosreve on x 22.9K followers

Created: 2025-05-12 03:32:25 UTC

GF Securities – Memory Sector: Downturn Approaching, HBM Pricing Pressured

– We downgrade the entire memory sector and assign an Underperform rating on Micron (MU US), SK Hynix (000660 KS), and SanDisk (SNDK US).

◾+ Sector slowdown and demand weakening intensifying – Following a bottom in 1Q23, the memory sector is projected to post XX consecutive quarters of improvement through 3Q25 — marking the longest upcycle since 2016. – However, a downturn is increasingly likely starting from 4Q25. Key reasons include: 1) Risk of a XX% tariff on electronics/semiconductors by the Trump administration 2) Deteriorating global macro conditions → smartphone shipment growth to turn negative, PC shipments limited to +1~2% 3) HBM pricing could also become a headwind

◾+ HBM and DRAM prices: Potential weakening from 3Q25 – As of CYQ2, memory pricing was stronger than expected (thanks to low smartphone inventories and preemptive restocking during the 90-day tariff waiver) – 2Q25 DRAM/NAND contract pricing: QoQ +67% expected – However, from 3Q25, price momentum is likely to slow due to weak demand and inventory pressure from servers and PCs: - Pricing increase of only around 0~5% or potentially flat - This flat trend may persist through 4Q25 ◾+ Samsung’s entry to intensify HBM market competition – Samsung is preparing to qualify HBM3e-12Hi with NVIDIA (possibly by June) – NVIDIA is delaying 2026 HBM3e pricing negotiations pending Samsung’s qualification – Samsung’s market entry in 2026 may trigger HBM4 price declines - Currently, HBM4 is priced at a XX% premium to HBM3e-12Hi - CXMT’s DDR5 production ratio also expected to reach XX% by end-2025 ◾+ Stock preference – 1st: Micron > 2nd: SanDisk > 3rd: SK Hynix - Micron: U.S.-based production → potential beneficiary of tariffs; gaining share in AMD/AWS - SanDisk: Focused on NAND → less exposed to HBM, relatively defensive - SK Hynix: Over XX% of DRAM revenue from HBM, but high exposure to HBM pricing pressure creates downside risk

✅ Conclusion: The memory sector is likely to peak in 3Q25, with a potential slowdown thereafter. HBM pricing headwinds and renewed U.S. tariff risk are expected to weigh on medium- to long-term valuations. Among covered names, Micron is viewed most favorably, while SK Hynix remains relatively conservative due to its large HBM exposure.

XXXXXX engagements

Related Topics $000660ks rating agency $1776hk